Japanese container shipping line Ocean Network Express (ONE) is utilizing a portion of the profits accumulated in recent years to accelerate the development of its own global port network.

The Singapore-headquartered ocean carrier has officially announced the signing of a share purchase agreement to acquire a 30% ownership stake in Hutchison Laemchabang Terminal Limited (HLT) in Thailand. This strategic move comes swiftly on the heels of a recent stake acquisition deal at a terminal in Busan, South Korea. Currently, the financial value of the transaction has not been disclosed by the parties involved.

Commenting on this transaction, Hiroki Tsujii, Managing Director of ONE’s Global Network and Product division, stated: “By deepening our partnership with Hutchison Ports, customers can benefit from enhanced reliability and efficient solutions within this essential trade hub.”

ONE’s acquisition of the stake in Laem Chabang occurs against the backdrop of the Hutchison Group actively seeking to sell off its port terminals worldwide for over a year.

]]>

Ocean carrier Hapag-Lloyd has issued an official advisory regarding the implementation of a General Rate Increase (GRI) for shipments moving from the East Coast of South America (ECSA) to the West Coast of South America (WCSA).

According to the notice, this rate hike will cover all types of cargo, including dry, refrigerated (reefer), and special equipment containers. The specific surcharge quantum is set at $200 per container.

The new GRI regulation will officially take effect starting May 1, 2026, and will remain in place until further notice.

Explaining this move, a Hapag-Lloyd representative stated that the rate adjustment is necessary to accurately reflect current market conditions. This surcharge will be applied universally to all containerized shipments flowing on the designated trade lane.

]]>

The cascading effects of the Middle East conflict have transformed routine aviation procurement and logistics into highly dynamic, risk-sensitive operations, demanding continuous coordination among suppliers, operators, and MRO service providers.

The Macro Picture of Operational Airspace

As of late March 2026, the central Middle East flight corridor has essentially ceased operations for regular commercial flights.

Following drone and missile incidents in the UAE and Qatar, the vast majority of regional airspace over Iran, Iraq, Kuwait, and Syria has been closed. Meanwhile, adjacent areas like Israel, Bahrain, the UAE, Qatar, Saudi Arabia, and Oman are operating under varying degrees of restrictions, requiring conditional clearances or the use of contingency routing. Even where airspace remains technically open, flight operations are strictly controlled with limited entry and exit points, stripping away scheduling flexibility and forcing heavy reliance on approved flight corridors.

Consequently, air traffic and Asia-Europe transport flows are now heavily concentrated on two highly constrained routing strategies:

● The Southern Route (via Egypt, Saudi Arabia, Oman): Offers the most viable continuous flight path but increases distance, prolongs flight times, incurs higher fuel burn, and faces the risk of navigational interference (jamming/spoofing).

● The Northern Route (via the Caucasus and Afghanistan): Presents its own set of hurdles, including complex coordination requirements and limited air traffic services (ATS) in certain segments, necessitating extreme caution in flight planning and contingency procedures.

Both options add hundreds of miles compared to standard Gulf routings, directly driving up block times and operating costs across both passenger and freighter networks. Concurrently, major airlines have slashed or suspended services to key regional destinations, leading to tens of thousands of canceled flights.

For instance, Cathay Pacific has extended its suspension of passenger flights to Dubai and Riyadh until May 31, reallocating capacity to European long-haul routes. A slew of other major names – including Aegean Airlines, airBaltic, Air Canada, Air France-KLM, Delta, IAG, Lufthansa Group, Singapore Airlines, Turkish Airlines, and Qatar Airways – have simultaneously announced flight cancellations, suspensions, or significant scale-backs of operations through this region spanning several months.

As a result, traditional commercial transport routes for aviation components have been forced to divert through longer, less efficient flight corridors, introducing delays and volatility into a network that was once optimized to the highest degree.

Fuel Price Shock Hits the Supply Chain Directly

The Strait of Hormuz, which previously saw around 20 million barrels of crude oil and petroleum products pass through daily in 2025, is now largely closed to commercial shipping, slashing transit volumes by 70–80%. This disruption has sent global fuel prices skyrocketing.

In the aviation industry, where fuel accounts for roughly 20–35% of operating costs, this impact is particularly severe. Jet fuel prices have surged over 60% since late February 2026 (from approximately $87 to $150–200 per barrel), inflicting immediate financial pressure on operators.

The fuel shock is also dictating maintenance decisions. Airlines are deferring shop visits for non-critical maintenance items to preserve liquidity, attempting to maximize the time-on-wing for engines and components.

Rerouting only exacerbates this challenge. Adding two hours of flight time on long-haul sectors translates to burning roughly 20% more fuel, all while paying an 80–100% premium per gallon. This risk is especially brutal for airlines without fuel hedging contracts, who are forced to procure fuel at exorbitant spot prices.

The Fracture of Transit “Mega-Hubs”

The Middle East has long been the nucleus of the global aviation system, serving not only as a transit corridor but also as a centralized “mega-hub” for both cargo operations and MRO services.

Cargo Network Congestion: On the freight front, the Asia-Europe corridor accounted for 21.5% of total global air cargo volumes in 2025. International airports like Dubai and Hamad (home base to Qatar Airways Cargo’s fleet of thirty Boeing 777F freighters) play a pivotal role. Disruptions at these hubs reduced global air freight capacity by approximately 22% in mid-March, while freight rates quadrupled compared to pre-conflict levels.

The capacity slump has intensified the competitive heat for belly-hold space and dedicated freighter payloads. For aviation parts suppliers, consolidating shipments, prioritizing high-value components, and establishing forward-stocking locations have become matters of survival. Transit times for aviation parts have increased by an estimated 20–40%, directly impacting time-critical shipments such as engine rotables, life-limited parts (LLPs), and avionics systems. Even a minor delay can result in Aircraft on Ground (AOG) situations or deferred maintenance.

MRO Infrastructure Under Extreme Pressure: Simultaneously, the region’s MRO infrastructure – valued at approximately $10.55 billion in 2026 with 25–30 Tier 1 providers such as Emirates Engineering, Etihad Engineering, Sanad, and Joramco – has been heavily impacted. Due to prolonged transit times and the fracturing of inbound component flows, MRO providers face immense difficulties in planning workloads and meeting Turnaround Time (TAT) commitments.

Faced with this predicament, some operations are gradually shifting to lower-risk regions such as Turkey and specific territories in Saudi Arabia. This immediately overloads these alternative locations, extending wait times and pushing turnaround schedules into future maintenance cycles.

Stranded Fleets and Materials: The Dual Cost Puzzle for Airlines

In this highly constrained environment, the phenomenon of stranded fleets and materials is becoming increasingly prevalent. Aircraft, engines, and components, rather than undergoing maintenance cycles to quickly return to service, are sitting in storage or trapped at MRO facilities for extended periods due to logistical, regulatory, and geopolitical barriers. Controlled preservation and storage consume thousands of dollars per unit, not to mention insurance and facility management costs.

Concurrently, airlines are under pressure to source alternative capacity at escalating rates, creating a dual cost burden. The situation is further aggravated by war risk insurance premiums, which have shockingly spiked by 50–500% in areas adjacent to the conflict zone.

Even when opportunities for recovery arise, repositioning fleets and materials remains incredibly costly and complex due to squeezed air freight capacity and limited routing options.

Proactive Adaptation Strategies

Even before the conflict escalated, operators were grappling with immense pressure regarding parts supply, MRO capacity, and supply chain reliability. The current geopolitical landscape is truly testing the endurance of the entire industry.

Core priorities right now include: establishing real-time inventory visibility, forward-stocking critical rotables and consumables, consolidating shipments, and optimizing dynamic routing across multiple hubs. To realize this, the adoption of digital supply chain management platforms is no longer optional; it is the vital “key” enabling operators to pivot flexibly and mitigate risks to the absolute minimum amidst the eye of this volatile storm.

]]>

In the event of a federal government shutdown, most essential freight operations are not expected to be affected. This is because the agencies operating these programs are often funded by separate mechanisms such as the Highway Trust Fund, or their employees are considered “essential” and will continue working.

However, this year, the Trump administration has threatened to use the shutdown as a pretext for further federal staff cuts, creating uncertainty about the extent of the impact on government employees, including those working at agencies under the U.S. Department of Transportation (DOT).

Jameson Rice, a transport attorney and partner at the law firm Holland & Knight, said: “The Department of Transport’s specialized agencies are largely responsible for safety functions, so whenever you cut from there, you risk reducing safety. That might not be felt immediately, but it will be in the long run.”

Essential Operations Remain Ongoing

According to the latest contingency plans, short-term safety functions related to domestic freight transport will continue, including:

- Road inspections conducted by the Federal Motor Transport Safety Administration (FMCSA).

- Rail accident investigations and safety recommendations by the Federal Railroad Administration (FRA).

- The U.S. Maritime Administration’s (MARAD) ship and port infrastructure security programs will continue to utilize “remaining budget balances.”

- Inspection of imported goods at land and sea borders is handled by the U.S. Customs and Border Protection (CBP), with approximately 93% of personnel retained.

- Ship inspections and port security are performed by the U.S. Coast Guard, with approximately 95% of personnel retained.

Risk of Delays from Other Agencies

While most CBP personnel are considered essential, this may not be true for other agencies that also oversee cargo inspections, such as the Food and Drug Administration (FDA), the Environmental Protection Agency (EPA), the Department of Agriculture (USDA), and the Consumer Product Safety Commission (CPSC). Activities such as on-site investigations, product testing, and recalls by the CPSC could be halted, potentially disrupting the supply chain.

Cindy Allen, an international trade consultant and former CBP executive, shared: “What is sometimes not considered essential is that additional inspections of shipments may be required and carried out by government agencies other than CBP.”

“So, products subject to government oversight may require additional review or inspection which could be affected, meaning there is a potential for slowing down the flow of goods,” she added.

Specific Impact on Regulatory Agencies

- Federal Maritime Commission (FMC): Will be heavily impacted. According to the plan, all “work aimed at advancing the agency’s mission to ensure a competitive and reliable international shipping supply system, support the U.S. economy, and protect the public from unfair and fraudulent practices” will be halted.

- Surface Shipping Board (STB): Activities related to processing applications, filing legal documents, and most litigation are likely to be suspended. This could impact the timeline for reviewing the $85 billion merger between Union Pacific and Norfolk Southern.

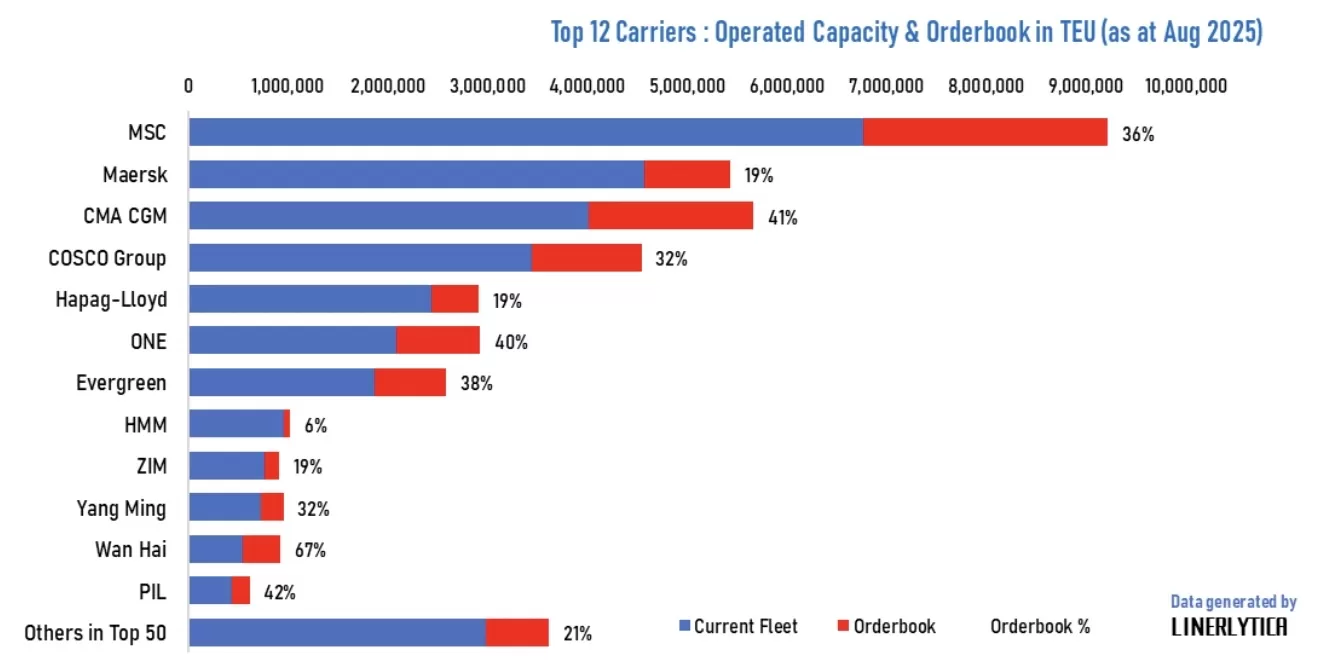

Container Shipbuilding Orders Exceed Historical Limits

According to the latest data from Linerlytica, the number of new container shipbuilding orders globally has reached 10.4 million TEU. This is an unprecedented figure in the history of the container shipping industry, pushing the orderbook-to-fleet ratio to 31.7% – the highest since 2010.

This means that for every three container ships currently in operation, one new ship will be delivered in the next few years. This rapid fleet growth raises the question: will the market have enough demand to absorb this enormous amount of capacity?

Comparisons from other sources show discrepancies, but all revolve around record highs:

- Clarksons Research and Alphaliner recorded a total of approximately 9.87 million TEU in orders.

- Clarksons added that, this year alone, the number of new contracts signed reached 275 vessels, double the average of the past 10 years.

These figures indicate that shipping lines are still aggressively expanding their fleets, despite the less-than-optimistic global demand outlook.

Concerns about a cycle of oversupply

Linerlytica issued a rather clear warning:

“The last time the order rate exceeded 30% was during the period 2004–2009. As a result, the container shipping industry experienced a prolonged period of overcapacity for a decade.”

This scenario is at risk of repeating itself. Besides the vessels already under contract, over 1 million TEU from pending orders will join the fleet before the end of the year. This further exacerbates the supply-demand imbalance.

Market data illustrates this discrepancy:

- The global container fleet currently stands at 145 points, compared to 100 in 2019.

- Container transport demand during the same period only reached 113 points, and even including the impact of many ships having to detour around the Cape of Good Hope, the figure only increased to 130 points.

- This means that transport capacity is increasing more than twice as fast as actual demand. Unless there is an unexpected boost in global trade, this surplus will persist in the market until at least 2029.

Freight rates face heavy pressure

One of the most direct and obvious consequences is that freight rates are unlikely to remain stable. The Xeneta freight analysis platform indicates that, although freight rates may fluctuate upwards due to geopolitical factors (e.g., tensions in the Red Sea forcing many ships to take longer detours), the core issue remains global oversupply.

- Supply: continuously expanding due to a surge in new orders.

- Demand: recovering slowly, insufficient to absorb the added capacity.

In this context, shipping companies are forced to consider cutting operating capacity or accepting fierce price competition to retain customers. This leads to the risk of a new “freight price war”—something the entire industry wants to avoid but is very difficult to control.

The Challenge for Leading Shipping Companies

The top 12 largest container shipping companies in the world (as of August 2025) currently control the majority of global capacity. With the continuous addition of new vessels, they face a double challenge: expanding their network to utilize resources while simultaneously adjusting capacity to avoid further exacerbating the oversupply situation.

Financially strong shipping companies can weather the storm in the long term, but smaller companies or those heavily reliant on short-term freight rates will be severely affected. This could lead to a wave of restructuring or mergers in the coming years, similar to what happened after the 2008-2009 crisis.

Conclusion

The record number of container shipbuilding orders brings optimism to shipyards and reflects the confidence of shipping companies in long-term demand. However, behind this boom lies an undeniable reality: supply is exceeding demand at an alarming rate.

Without an effective balancing act, the container shipping industry could fall into a vicious cycle: overcapacity, plummeting freight rates, and eroded profits. These developments will continue to have a profound impact on the entire global supply chain for years to come.

Interlink will continue to monitor and update on major fluctuations in the container shipping market, helping businesses and customers proactively respond and optimize their logistics strategies in the current volatile environment.

]]>The Trans-Pacific shipping market continues to see a sharp decline in container freight rates. According to the latest data from Xeneta, spot rates from the Far East of Asia to the United States have fallen significantly since June, despite shipping lines’ efforts to reduce capacity.

- Far East → US West Coast: $2,098/FEU (down 3% from July 31st, down 62% from June 1st).

- Far East → US East Coast: $3,311/FEU (down 9% from July 31st, down 53% from June 15th).

Since the end of June alone, freight rates to the US East Coast have fallen by another 9%, to $2,015/FEU.

Cause: Oversupply and weak demand

Peter Sand, Director of Analysis at Xeneta, noted that shipping lines have significantly increased blank sailings to limit supply. From 30,000 TEU/week (June 22nd), this figure has risen to 57,000 TEU/week (August 1st).

However, the global overcapacity of the container fleet and the gloomy demand forecast make maintaining high freight rates difficult, “like trying to block the flow of water.”

Consequences: Port congestion and container backlog in China

The increased number of cancellations has caused severe congestion at several major Chinese container ports. Many containers are backlog at the terminals, with shippers using the ports as temporary storage while waiting for space on ships.

This not only affects shipping schedules but also increases storage costs, impacting the global supply chain.

Comparison of Freight Rates in Europe and the Mediterranean

Besides the North American route, Xeneta also recorded freight rate trends from the Far East to Europe:

- Far East → Northern Europe: US$3,330/FEU, stable after a 78% increase (May 31–July 1) and a 2% decrease since then.

- Far East → Mediterranean: US$3,372/FEU, down 7% from July 31 and down 26% since June 15.

The price difference between these two routes is now only US$42/FEU, compared to US$1,765 on June 1.

According to experts, if the oversupply and weak demand continue, container freight rates on the Asia-North America route will continue to fall in the coming months. Shipping lines may continue to adjust capacity, but the likelihood of reversing the current trend is very low.

]]>So what’s special about this new order? What do Vietnamese businesses exporting to the U.S. need to prepare? Let’s analyze it in detail in the article below.

Main Contents of the Executive Order of July 31, 2025

According to the new Executive Order signed by President Donald J. Trump, notable changes include:

1. Additional tariffs based on the principle of “reciprocity”

The United States will apply additional ad valorem (a percentage of the value of goods) tariffs to goods from countries with tariffs, technical barriers, or trade policies that are disproportionate to those of the United States.

Example:

- Goods from Vietnam will be subject to an additional 20% tax.

- India: 25%

- Thailand: 19%

- EU: Additional tax is adjusted flexibly depending on the type of goods (minimum 15%)

2. Measures to combat tax evasion through transshipment

Any transshipment aimed at tax evasion will be heavily penalized:

- A 40% additional tax will be applied.

- Other additional penalties and recovery charges as per federal law.

- No mitigation or exemption will be considered.

3. Changes to the HTSUS tariff schedule

The United States Classification System (HTSUS) will be revised to clearly reflect the tax rates by country and product group. These revisions will take effect 7 days after the date of signing.

What should Vietnamese businesses exporting to the US be aware of?

1. Increased Costs

With an additional 20% tariff, the total cost of exporting goods to the US will increase significantly, especially for sectors such as:

- Textiles

- Wood and wood products

- Consumer electronics

- Processed foods

2. Tighter Customs Inspections and Procedures

Goods from Vietnam will be subject to stricter inspections regarding origin and the possibility of transit through a third country to evade taxes.

3. Risk of Supply Chain Disruptions

With stricter regulations, if businesses are not well-prepared in terms of paperwork, declarations, and shipping procedures, the risk of delayed customs clearance or return of goods is entirely possible.

Interlink – Safe and Optimal Logistics Solutions in the Context of Changing Policies

At Interlink, we understand the complexity and risks in export operations in the post-pandemic era and geopolitical instability. Therefore, we are committed to supporting businesses in:

Advising on and updating the latest tax policies:

We closely monitor executive orders, HTSUS tariff schedules, and changes related to import and export.

Optimizing shipping routes:

Advising on routes to avoid risky transshipment, ensuring correct country of origin, and optimizing transportation costs.

Supporting the preparation of complete and valid customs documents:

Helping businesses ensure transparency and compliance with the law when exporting to the United States.

Conclusion

The new US Executive Order serves as a strong warning to countries with unbalanced trade relations. In this context, Vietnamese businesses need to proactively grasp information, review export processes, and work closely with reputable logistics providers like Interlink to minimize risks and maintain a stable flow of goods to the US market.

]]>Asia-Europe Container Rates: Slightly Cooling Down, But Not Stable

The recently published World Container Index (WCI) by Drewry shows that freight rates on the Shanghai-Rotterdam route have decreased by 2% compared to the previous week, to US$3,384/40ft container. This is the first time in over a month that rates have shown signs of adjustment after a prolonged upward trend.

However, the market is reflecting conflicting trends. The SCFI index remained high at $3,996/container, while Xeneta’s XSI stabilized at $3,393. Notably, Freightos’ FBX index increased by 14% to $3,522/container – indicating inconsistency in the container freight market.

Many freight forwarders assess that the market is currently sideways, with some shipping lines beginning to slightly reduce prices to maintain competitiveness. Except for a few hotspots like Xiamen port, most shipments are still moving smoothly, with no signs of serious congestion.

Port Congestion in Europe: A Trigger for New Changes?

Despite seemingly stable freight rates, the risk of port congestion in Northern Europe is clearly increasing. According to Peter Sand, Director of Market Analysis at Xeneta, disruptions at major ports such as Hamburg, Rotterdam, and Antwerp could last until the end of 2025.

Shipping companies have begun to take countermeasures such as skipping ports of call, changing routes, and consolidating shipments to shorten transit times and minimize the risk of delayed deliveries. However, these measures also increase complexity in the supply chain and create additional costs for shippers.

Frequency Rates on Other Routes Also Fluctuate Significantly

Not only the Asia-Northern Europe route, but other shipping routes have also seen significant changes:

- Asia-Mediterranean Route: WCI recorded a 7% decrease to $3,491/40ft container. This is the first time in many years that the Mediterranean route has had lower rates than the Northern Europe route.

- Asia-North America Route: Shanghai-Los Angeles decreased by 8% to $2,931; Shanghai – New York freight rates fell 5% to $4,839/container. Freight rates to the US West Coast have dropped 51% in just over a month – primarily due to the impact of new tax policies and a decline in pre-ordered cargo.

- Transatlantic Route: Rotterdam – New York freight rates also reversed course, falling 6% to $1,990/container.

Sea Freight Market: Challenges Driven by Information

In a period of market instability, staying updated on freight rates for Asia-Europe and other key routes is crucial for import and export businesses. Changes in consumer behavior, geopolitical pressures, and port congestion have made global supply chains more unpredictable than ever.

Interlink – with over 15 years of experience in international shipping – proactively updates market information, advises on optimal solutions, and ensures timely delivery under all circumstances. We help our clients stay one step ahead in the face of change, thereby minimizing costs, avoiding risks, and ensuring efficient supply chain operations.

]]>During the exchange, President Trump highly appreciated Vietnam’s commitment to opening its market, especially to American goods such as large-displacement automobiles. He also affirmed that the US would significantly reduce the tariffs currently applied to many types of goods exported from Vietnam to the US.

However, according to experts, the key issue now is waiting for detailed information on specific tariff rates, classification and application to each type of goods, as well as a clear definition of “transit goods”.

Several scenarios regarding tax policy are predicted.

Mr. Nguyen The Minh – Director of Individual Client Analysis at Yuanta Securities Vietnam – believes that the US could implement one of two options:

- Applying a uniform tax rate to all goods.

- Establishing different tax rates depending on the localization rate and origin of raw materials.

According to Mr. Minh, the new tax policy is likely to reduce the US’s dependence on goods from China. One highly anticipated scenario is that the US will impose a tax rate of approximately 20% on goods manufactured in Vietnam, with the specific rate depending on the percentage of raw materials imported from China.

Although the 20% rate may be higher than initially expected (10–15%), according to Mr. Minh, this is still a positive sign, helping Vietnamese goods maintain a competitive advantage over China and some other countries.

The issue of “transit goods” raises concerns.

Regarding information that the US may impose tariffs of up to 40% on goods deemed to be in transit through Vietnam, Mr. Minh stated that the crucial issue is how the US defines “transit” and the specific regulations involved. Vietnam also needs to develop a negotiation plan to mitigate the impact if this scenario occurs.

Following the announcement of tariff negotiations, the stock prices of some US companies such as Nike, Apple, and footwear manufacturers increased, reflecting positive investor sentiment following the preliminary results.

Currently, no specific tariff rates have been announced for each industry group. However, the move from the US shows a clear willingness to adjust tariffs on Vietnamese goods.

Nevertheless, to fully assess the impact on foreign direct investment (FDI), it is necessary to continue monitoring the tariff policies that the US will apply to other countries in the region.

Academic Opinions

Associate Professor Pham The Anh – Head of the Economics Department, National Economics University – stated that if the US applies flexible tariffs based on domestic content, this would be a positive signal for Vietnam’s export growth. He assessed that if the tariff framework of around 20% is accurate, it would still be an “acceptable” figure in the current context.

Meanwhile, countries like India and Japan are also rushing to negotiate trade agreements with the US, but still face many obstacles, especially in the agricultural and automotive sectors.

What should logistics businesses do in the face of this wave of change?

For logistics businesses, especially those specializing in exports to the US like Interlink, this is a “golden” time to optimize transportation solutions, standardize documentation, and build a clear and transparent supply chain system.

Interlink currently supports hundreds of Vietnamese businesses in the following processes:

- Consulting and processing Certificates of Origin (CO), helping goods meet new US tariff requirements.

- Optimizing cross-border shipping: from consolidation, warehousing, booking to door-to-door delivery in the US.

- Analyzing supply chain strategies to avoid transshipment risks and ensure compliance with new regulations.

What opportunities are there for export businesses?

The US is currently one of Vietnam’s largest export markets, with export value reaching tens of billions of USD annually. The tariff reduction will:

- Increase the competitiveness of Vietnamese goods compared to China and other countries in the region.

- Promote FDI into domestic manufacturing industries such as textiles, electronics, and wood products – leading to a significant increase in logistics demand.

- Create momentum for breakthroughs for Vietnamese businesses, especially those already prepared in terms of documentation, logistics systems, and market strategies.

Interlink – Your Trusted Logistics Partner in the New Wave of Trade

With over 15 years of experience in international logistics and a wide network of partners in the US, Interlink is ready to support Vietnamese businesses in overcoming tariff barriers, optimizing costs, and accelerating exports.

If you are a business exporting to the US or planning to expand your market in the near future, don’t miss this “big wave.” Policies may change, but the advantage will be with those who prepare in advance.

]]>Despite military tensions between Israel and Iran entering their fourth day with multiple missile strikes, two key Israeli ports – Haifa and Ashdod – remain operational.

Over the weekend, missiles from Iran targeted the Haifa area, home to one of the region’s busiest container ports, along with a nearby oil refinery. However, there were no reports of serious damage or disruption to port operations.

Notably, the Haifa port handles up to 30% of Israel’s total imports and is currently operated by the Adani Group (India). ZIM, a shipping company based there, confirmed that ships are arriving on schedule and bookings to and from Israel are being processed as usual.

Israel’s Haifa Port

Middle East Logistics Risks Remain High

While ports haven’t been directly affected, the entire Middle East region is experiencing a significant increase in maritime risks. According to the Joint Maritime Information Centre (JMIC), the main threat now doesn’t come from physical attacks, but from signal disruptions and navigation safety issues:

- AIS (Automatic Identification System) spoofing

- GPS jamming, severely impacting navigation

- This situation is worsening in the waters near Bandar Abbas (Iran) and the Strait of Hormuz.

In particular, the Iranian Parliament has officially discussed the possibility of closing the Strait of Hormuz – a narrow but extremely important route for global shipping. If this scenario occurs, it could stifle 20% of the world’s oil and gas supply, causing a chain reaction shock to energy-dependent industries.

Chain Reaction: Containers, Oil & Gas, and Transit Networks

According to expert Jean-Paul Rodrigue (Texas A&M University), 30 million TEU containers per year move around the Hormuz region, mostly transit cargo – unrelated to oil and gas – but could be severely affected if the shipping route is disrupted.

Some notable developments at other ports in the region:

- Jebel Ali (UAE): still operating stably, no disruptions reported

- Salalah (Oman): experiencing disruptions due to weather (monsoon), unrelated to conflict

This is evidence of the fragility of the regional supply chain: a single link failing – whether military or weather-related – can have a chain reaction impacting the entire international logistics system.

Conclusion

Currently, Israeli seaports are maintaining stable operations and have not been affected by the conflict. However, the level of risk to shipping operations in the Middle East is increasing, especially on strategic shipping routes such as the Strait of Hormuz.

Import-export businesses need to continuously update market information and geopolitical scenarios to prepare flexible logistics plans and avoid being caught off guard if the situation becomes complicated.

]]>